{kind=link}

We are now nine months into the year, and unless Pakistani startups can secure significant deals in the last quarter of 2023, it appears that the year is not going to end on a high note. At this point, analyzing the data is more of a formality as the numbers are too small to provide any meaningful insights.

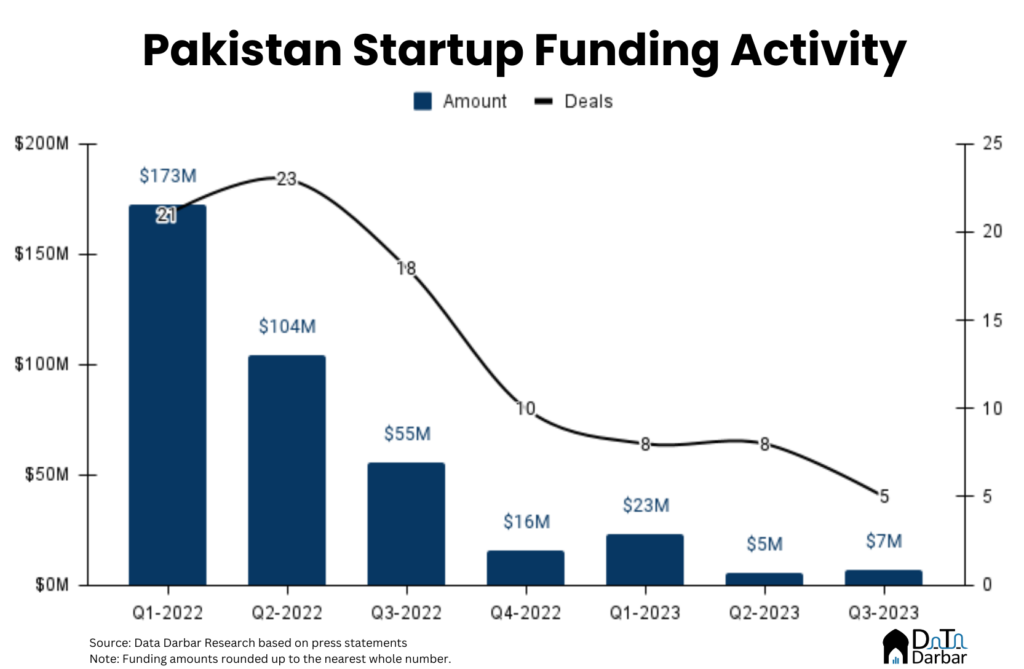

In any case, the investment in the third quarter has increased to $6.8 million from the $5.2 million raised in Q2-2023. While this represents a quarter-on-quarter increase of 30.8%, it’s worth noting that funding has dropped significantly by 87.7% compared to Q3-2022. This brings the total for the first nine months of 2023 to just $35.1 million, marking an 89.4% decrease when compared to the same period in the previous year.

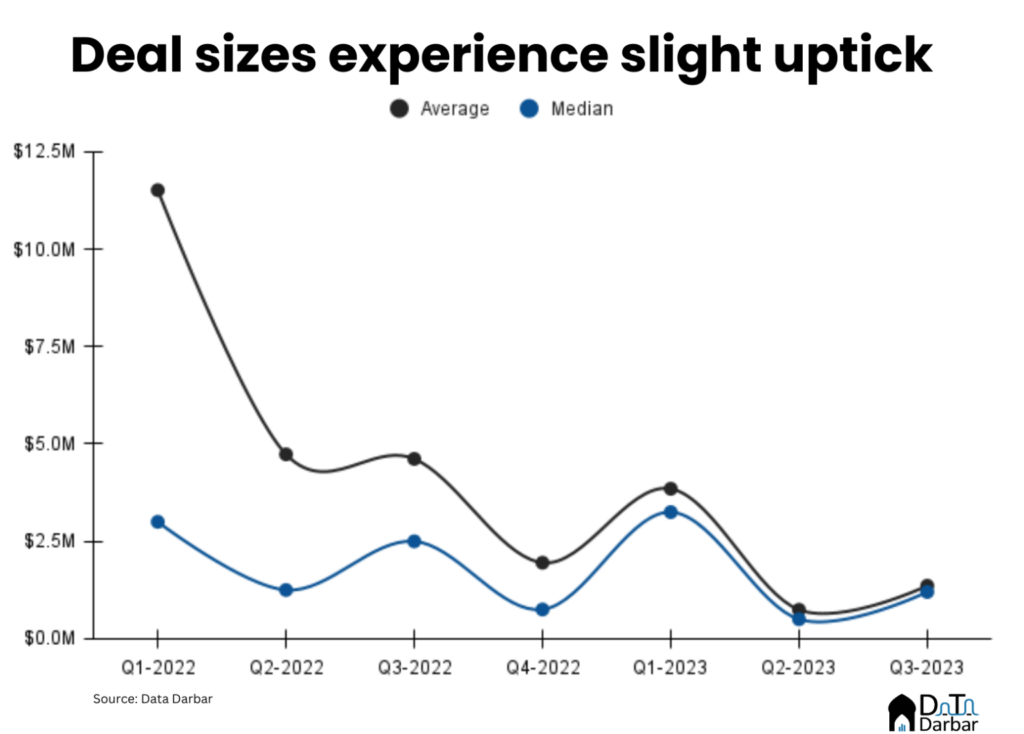

In terms of the number of deals, this quarter was again rather lackluster, with only five funding rounds announced. This represents a 50% decrease compared to the previous year and a 37.5% decline from the previous quarter. For the first nine months of 2023, there have been a total of 21 deals, which is essentially the same number as in Q1-2022 alone. Consequently, the average ticket size has decreased by 70.5% year-on-year, reaching $1.36 million in Q3-2023 from $4.26 million. Although this is an increase compared to the $742.9K in the last quarter, it’s still relatively low. So, there’s not much reason for celebration in this regard.

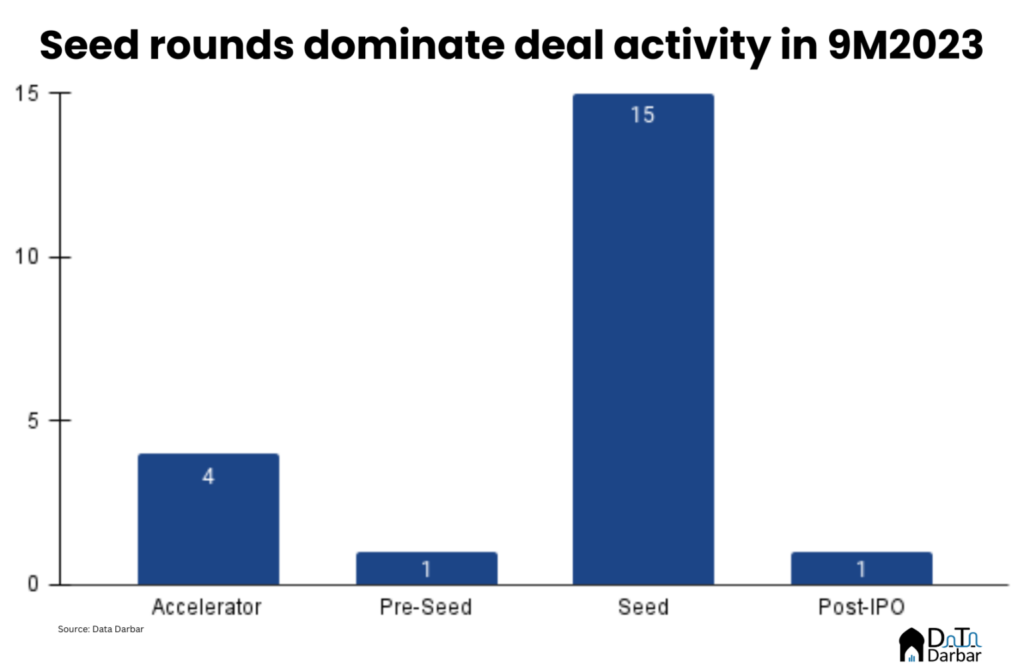

In terms of the stages of investment, all five startups in this quarter raised seed deals. In the first nine months of 2023, seed investments have been the most dominant, accounting for 15 out of the 21 deals. Notably, pre-seed investments, which were once quite common during the period when investors were eager to invest based solely on a pitch deck, have significantly declined. Nowadays, having some traction is almost a prerequisite.

During the quarter, each of the five deals was in different sectors. Edtech, thanks to Taleemabad, had the largest share with $2.6 million. However, the relatively small size of the investments in these different sectors over a three-month period makes it challenging to derive meaningful insights. Over the first nine months of 2023, fintech was the most dominant both in terms of the amount invested ($14 million) and the number of deals (7). Transport and logistics followed, with $11 million invested in four deals.

Indus Valley Capital was the only investor with two deals in the quarter, while Sarmayacar had one. Zayn VC, i2i Ventures, and Fatima Gobi did not announce any investments in Q3-2023, and each has only disclosed one investment each in 9M2023. However, this might also indicate that local VCs are making investments but not making many public announcements.

This underwhelming deal activity is not unique to Pakistan and is a broader feature of the venture capital landscape. In Q2-2023, global venture funding totaled $60.5 billion, the lowest since the first quarter of 2018, according to CB Insights. This means that the exceptionally high levels of investment observed after 2020 have subsided, and investment activity has returned to pre-Covid levels. Even traditionally robust markets like India are facing challenges, with Q3-2023 recording the lowest figures in the last five years.

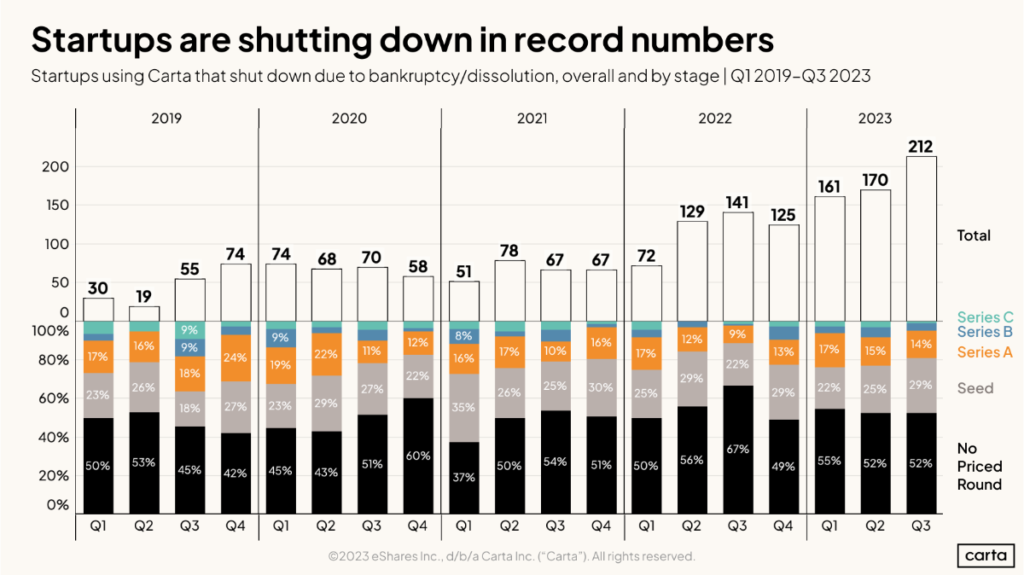

In summary, this quarter has been quite challenging, with the shutdown of Medznmore, one of the most well-funded companies, followed by Jugnu, which also halted its core operations. According to Carta’s database, this year has seen a record number of startup closures, indicating a global trend.

Even established companies like Zameen, which had experienced substantial growth until now, are starting to feel the impact. The only sectors that have performed well recently are those that largely depend on Pakistan’s structural imbalances, such as banks (due to fiscal deficits) and the energy sector (due to devaluation). For the rest of the sectors, there is no immediate relief in sight, and it will likely be some time before things take a turn for the better.